Exxon Mobil explores for crude oil and natural gas in wells, and also manufactures oil-related products. Its revenue contribution is about 50% derived from North America, with the other 50% coming from its global operations.

Disclosure: This is not investment or financial advice. I take no responsibility for anyone’s decisions regarding this.

Investment Catalyst

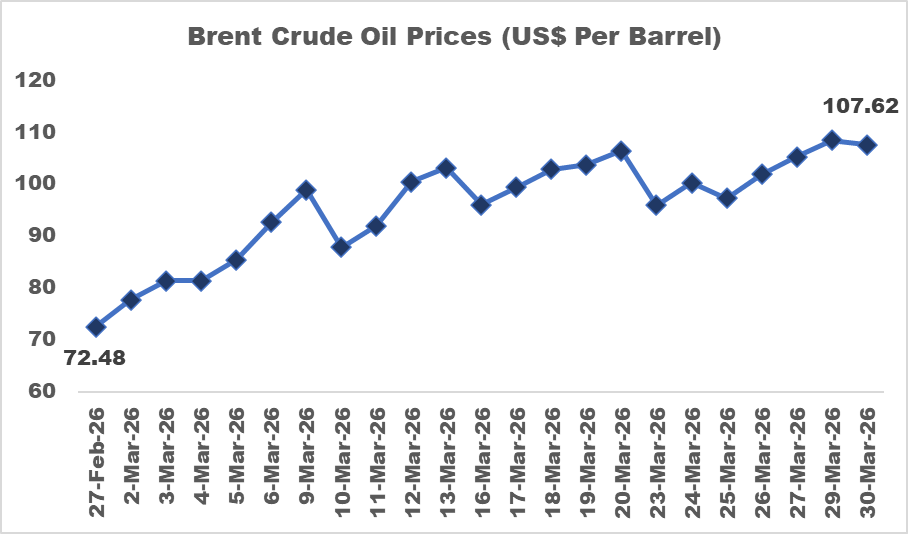

The Iran-Israel-U.S. conflict has sparked a global supply shortage of oil-related products in the market. The Straits of Hormuz, which enable the transportation of about 31% of the world’s supply is now being closed by Iran. As a result, oil prices have shot up considerably since the Iran conflict started at the end of February 2026.

Exxon Mobil, being an oil & gas company, stands to benefit from this uptrend in prices. However, this is primarily driven by the supply shortages caused by the conflict, which could be short-term. This article examines the longer-term fundamentals of the company and also its valuations.

#1: Financials have Grown But is Volatile

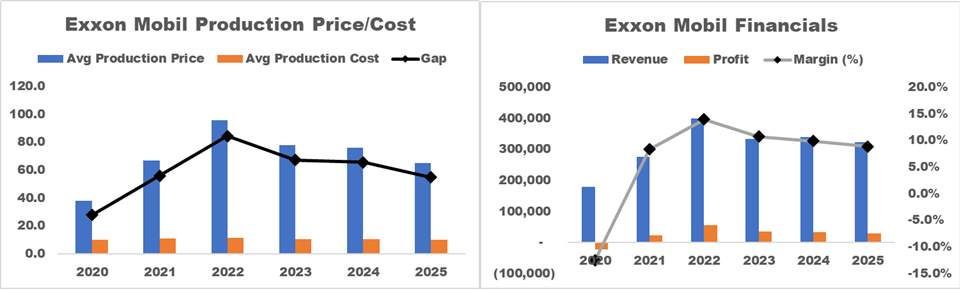

I look at two main financial metrics here – revenue and earnings. From 2021 to 2025, revenue grew at an annual rate of 3.7% to $323 billion. However, that growth has been unstable. Being an oil & gas company, it is exposed to the volatility of oil prices.

It registered a very strong growth of 57.4% and 42.8% in 2021 and 2022, respectively and reached its peak revenue level of $400 billion. This was due to the pandemic recovery and high oil prices from the Russia-Ukraine conflict. However, in 2023, revenue crashed by 16.7% to $333 billion, before climbing by 1.9% to $340 billion in 2024. Lastly, in 2025, due to weaker oil prices, revenue slid by 4.7% to $324 billion.

Its profit trend is more concerning. It has continuously declined from 2022 ($55.7 billion) onwards to $28.8 billion in 2025. This reflects the impact of lower oil prices on profit margins.

However, it also presents an interesting observation about its earnings trend if we look at its volume and average selling prices for 2026 as a whole.

#2: Financial Margins/Performance Driven Primarily by Prices

Exxon Mobil’s annual reports are thick to go through. But I went through 3 of them (2025, 2023, and 2022) to investigate the numbers driving their revenue and profit.

At its core, it publishes two main statistics that describe its demand and supply – production price and cost per barrel. Right off the bat, its production cost per barrel is very stable at around $10 to $11 per barrel over the years. It is the production price per barrel that swings wildly, as it should, as it follows global crude oil and natural gas prices.

I examined two trends here: 1) the ‘gap’ between production cost and prices, and 2) the revenue level and net profit margin of Exxon Mobil to tease out a meaningful trend to forecast 2026. Their trends should look alike.

Here’s an important observation. I think Exxon Mobil’s ‘breakeven’ price is at around $40 to $45 per barrel as evident by the year 2020. Production price was at $38, while production cost was at $10.2. Indeed, both trends are similar.

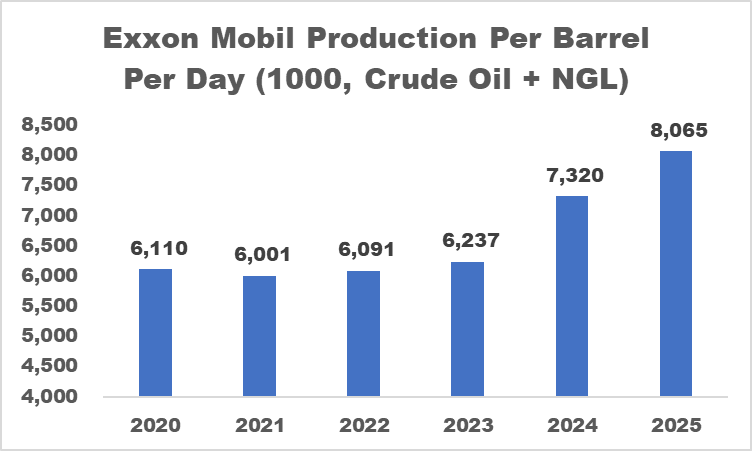

Mind you, Exxon’s production volume has consistently increased throughout the years (except 2021). So, it’s reasonable to conclude that price is the main factor that drives Exxon’s business.

I can see now why investors bought a lot of Exxon stocks when prices skyrocketed up. They see a repeat of a boost in financial performance for 2026 similar to the one in 2022.

- 2022: Production price rose from $67 per barrel in 2021 to $95.9 in 2022. Volume was flat at around 6 million barrels per day for both years. Revenue rose by 42.8% to its peak of $400 billion, while profit margin increased to 14%.

- 2026: Production price was at $65.2 per barrel in 2025, and Brent crude oil prices is now at $107.62 per barrel. This is a ‘larger’ gap that Exxon is looking at at least for the first 2 quarters of 2026.

In the next point, I will be doing some simple projections and a DCF model, and examine whether this valuation is fine compared to market valuations now.

#3: 1H 2026 Could Be Big for Exxon

Firstly, 61% and 40% of Exxon’s crude oil and natural gas liquid, and natural gas production is in North America (Canada included). It’s hard to properly estimate Exxon’s exposure in the Middle East as it’s bundled together into Asia and Africa. However, this means that many buyers will probably be buying from Exxon’s Non-Middle East operations and more specifically, the United States.

As its production has increased over the years, this places the company in a solid position to capitalise on this opportunity. It currently has a total proven reserves of 19.3 billion barrels that could see higher demand.

I will do some simple projections for 2026 as a whole based on oil price projections from EIA here. They see a higher average crude oil price of $80 for 2026 ($69 for 2025) as they are assuming that the Straits of Hormuz will reopen by the end of 1H 2026. However, 1H 2026’s average is around $90, which is high.

Here are my assumptions for the discounted cash flow (DCF) valuation for 2026

- Revenue growth: 30% (assuming both volume and price growth)

- Profit Margin: 10.8% (implied EBITDA margin of 20.4% in DCF)

For the rest of the years from 2027 to 2030, I will just assume its CAGR average of 3.7%, and the historical average EBITDA margin of 19.2%. Here’s the result.

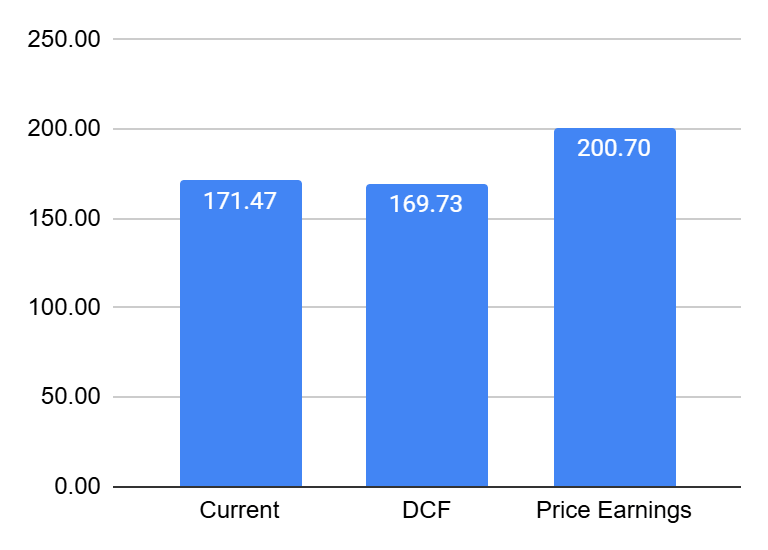

Based on the DCF valuation (Excel file here), Exxon does look fairly valued at the current stage. For the price-earnings assumption, I obtained its peers’ average price-to-earnings ratio of 30 times, and indicates that Exxon could trade at $200.7.

#4: For now, Exxon Valuations are ‘Fair’

Exxon Mobil’s share price has risen by 42% since the beginning of the year, which could mean that most of its upside has already been priced in.

And this is supported by the previous DCF valuation that its ‘fair’ price is at $170. From this perspective, I think investors are just waiting for 1Q 2026 results to come out to indicate that, indeed, revenue is growing and its margins are also increasing. The real test will come in 2Q 2026, and whether oil prices still remain above $80 or $90 per barrel.

#5: Long-term Economic Fundamentals Might Matter More

Once investors have moved past this conflict, long-term economic fundamentals will come into play. Exxon Mobil is, after all, the biggest U.S. oil & gas player, with close to $800 billion in market capitalisation. It services mostly North American clients.

For now, the American economy is chugging along steadily, with fears of a weaker job market. AI risks are still prevalent, with President Trump chastising Exxon recently, becoming a central risk to Exxon’s access to Venezuela (should it happen).

The global economy could also weaken with the ongoing oil supply disruptions, which could increase the cost of freight, transportation and electricity first, before feeding into everyday items. Inflation will become central again to the global economy. A long-term weakening of the global economy is inherently worse for Exxon Mobil, even though they have high average selling prices.