Container shipping and logistics isn’t the most sexy thing. Well, at least compared to the cutting edge AI companies that gets all the attention.

But I think it is the sleeper sectors and companies that are the most valuable. They are in the background. They don’t flaunt their achievements.

They are the silent backbone of the economy.

Those are my first thoughts when I read that MTT Shipping and Logistics (MTT) was listing in the Malaysian market.

But does it stand up to scrutiny? Is the biggest shipping and logistics player that guy?

Let’s find out. Here are 7 things that I want you to know about MTT Shipping and Logistics IPO.

#1: MTT is a Shipping and Logistics Company Primarily in Malaysia

MTT helps its clients/companies transport their products in bulk in containers from one place to another. It handles the logistics and warehousing side of it too.

To put it plainly, imagine a company gets an order for a lot of its products from Kuching. It makes the stuff in Selangor. It will contract a merchant or freight forwarder to come, pack and put the things into containers. Here’s where MTT will come into the picture. These merchants and freight forwaders will contract MTT to collect the containers, store them in their warehouse, put them on the freight ship, and transport them to Kuching. Once it reached Kuching, MTT will unload and store them at their warehouses, waiting for the merchants to come and collect them, and transport them to clients.

Currently, it has 24 ships (or container vessels) that service routes between West Malaysia and East Malaysia. It also charters out its ships to other companies. Other than Malaysia, it also goes on routes to countries like Brunei, China, India, Indonesia, Thailand, and Singapore.

MTT generally has about four main business segments – shipping operations (69% of revenue), vessel chartering (19%), dry bulk shipping (8.3%), and depot-related income (3.0%).

#2: Listing Proceeds to Buy More Ships

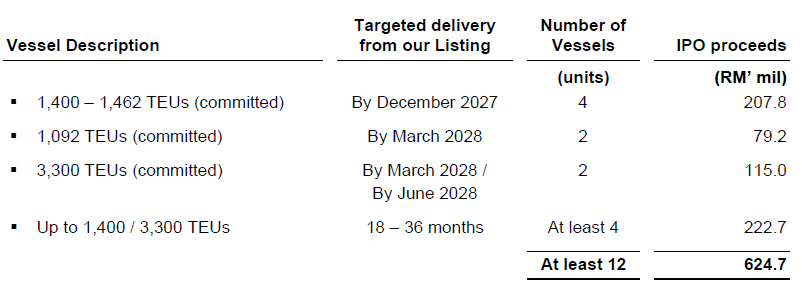

MTT is raising RM653 million for two purposes – buy new container vessels and pay for listing fees.

It is spending RM625 million to acquire 12 additional ships over the next 1.5 years. It is using RM402 million to pay for these ships that are scheduled for delivery between Dec 2026 and June 2028.

- Four ships with capacity of between 1,400 to 1,462 TEUs

- Two ships with 1,092 TEUs

- Two ships with 3,300 TEUs

The deposits for these ships have already been paid for. Furthermore, MTT intends to use the remaining IPO proceeds (RM223 million) to either build bigger capacity vessels (3,300 TEUs) or smaller ones (1,400 TEUs). It intends to source them by the end of 2Q 2026.

#3: Financial Growth has Been Mixed

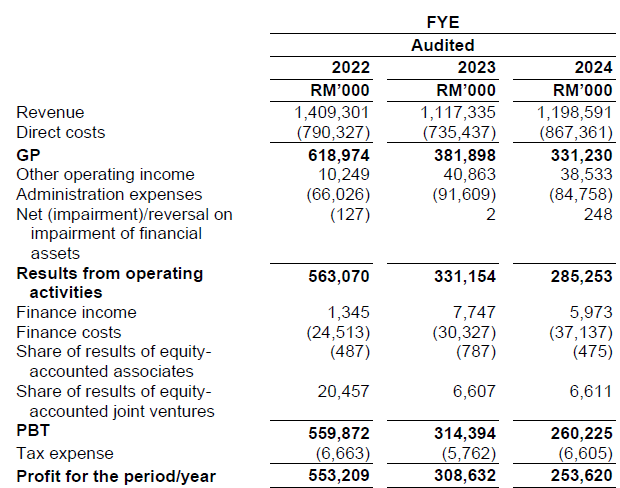

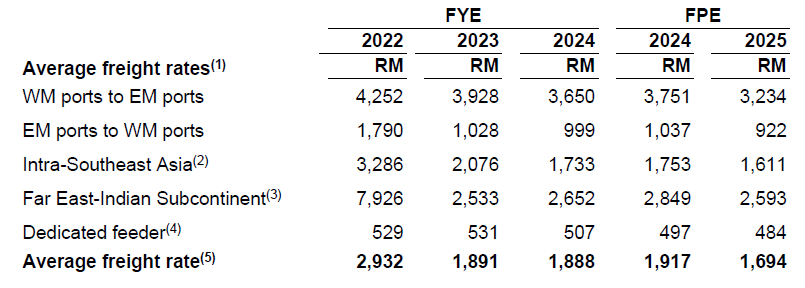

Let’s get this out of the way. MTT only published full-year results from 2022 to 2024, and 9 months of 2025. And if we just look at the annual results from 2022 to 2024, it will look like MTT is not doing too well, as revenue has declined.

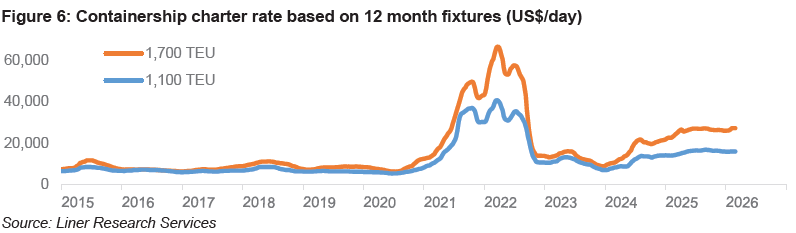

It seems like MTT reached its peak in 2022 and subsequently suffered. But context is always important in this case. The thing is, most shipping and logistics companies reached their peak performances in 2022 and declined after that. That’s because freight rates were at their highest during the pandemic from 2020 to 2022.

Here’s an example from COSCO Shipping – one of the biggest shipping company in the world.

MTT Shipping follows the same trend as most shipping companies in the world. So, we should properly interpret the results of MTT in the context of what’s happening in the industry. Based on its latest 9 months of 2025, MTT seems to be recovering again.

- Revenue is up by 10% to RM961 million.

- Profits are even higher by 24% to RM236 million.

There’s an important point to consider here. MTT is a scalable business that depends on the capacity of its shipping containers. The higher the capacity, the higher the profit margins. And it shows from its profit margins.

In 2022, when revenue was at its peak, MTT recorded a net profit margin of 40% (RM560 million / RM1,409 million). In 2023, revenue declined sharply, with net profit margin also declining to 28%.

What does this mean? In years when revenue is growing rapidly, expect profits to grow even stronger, resulting in higher margins. This makes sense if you consider the fact that a ship that carries about 40% of its capacity will make less profit compared to a ship that carries 90% capacity. For a journey, you still have to pay for staff, fuel and maintenance regardless of how much you are taking.

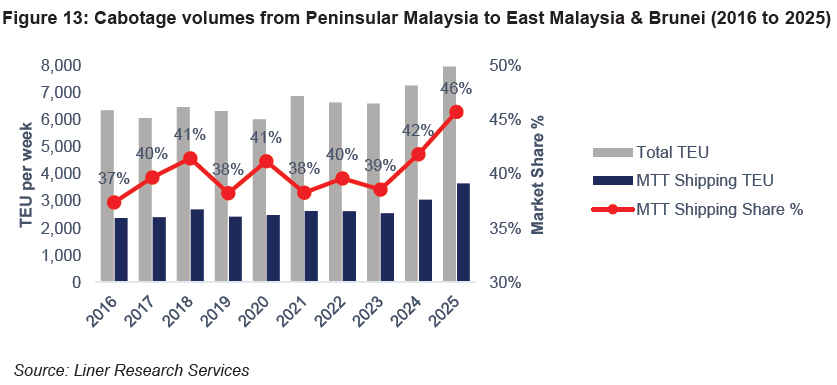

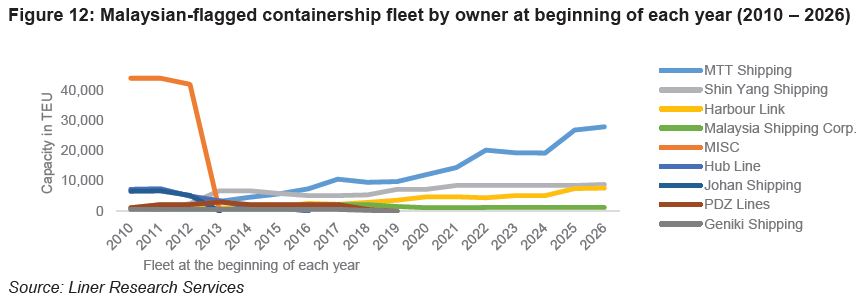

#4: MTT Is the Biggest Shipping Player on the West-East Malaysian Route

There are currently four major players in the Malaysian shipping logistics industry that runs from West Malaysia to East Malaysia, with MTT Shipping commanding

- 61% of TEU capacity and

- 47.2% of the Malaysian-flagged containership fleet unit.

Yes, MTT is the leader. And it has rapidly gained market share in the past couple of years. In 2019, it had about 38% of the cabotage volume. That had increased to 46% in 2025.

Its closest competitors are Shin Yang and Harbour Link, where the route has seen significant exits from players such as MISC in 2013, Johan Shipping (2012), Hub Line (2015), PDZ Lines (2017), and Geniki Shipping (2017). The shipping and logistics are notoriously hard to penetrate, considering Malaysia’s cabotage protectionism policy. However, since 2017, foreign carriers have been allowed to service the routes between West and East Malaysia, where Maersk and RCL have entered the market. However, their market share remains low at 5%.

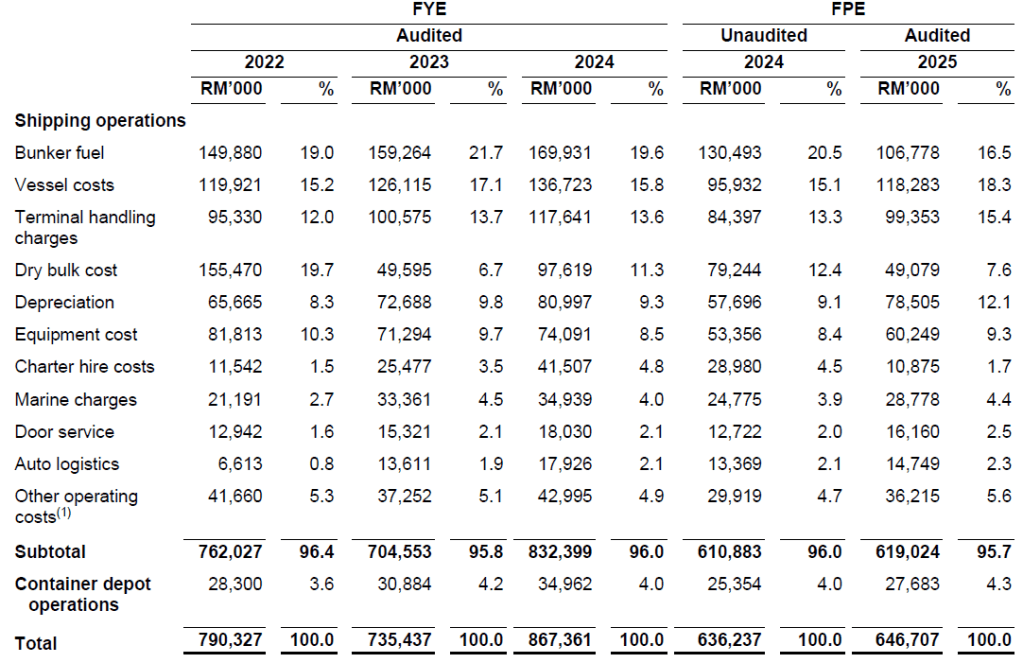

#5: Understanding its Cost Structure

I don’t do this often, but I feel that cost structure is becoming an important piece of the puzzle for most of the companies that I am analysing. The Iranian conflict has become a key risks for shipping companies around the world, as they depend heavily on fuel to run their ships.

In economics, costs are divided into two – fixed and variable. If you don’t understand this, don’t worry. Fixed costs refer to costs you have to pay regardless of your operations. Think of the rent of your shoplot as fixed, as you still need to pay it no matter how much revenue you make. Variable costs are expenses you incur to run your operations. Fuel is an example of it. If your ships are not travelling, you don’t use fuel.

Here is a high-level view of the cost structure of MTT:

There are essentially 5 items that we need to look into – bunker fuel, vessel costs, terminal handling charges, equipment cost, and dry bulk costs.

Vessel costs make up the biggest component at 18.3% of total costs, and are used to operate ships. It includes crew cost/salary, maintenance, insurance, and ship management fees. Bunker fuel, meanwhile, is the fuel to run the ships and comes at 16.5% of the total cost. Terminal charges come third with 15.4%, and that includes the fees paid to ports to lift containers into and off the ships.

Equipment costs make up about 9.3% of total costs and include costs related to containers, such as repairs, storage, and terminal handling fees. Lastly, dry bulk costs are related to the freight fee for dry bulk shipment.

#6: Risks From Fuel and Ship Maintenance Costs

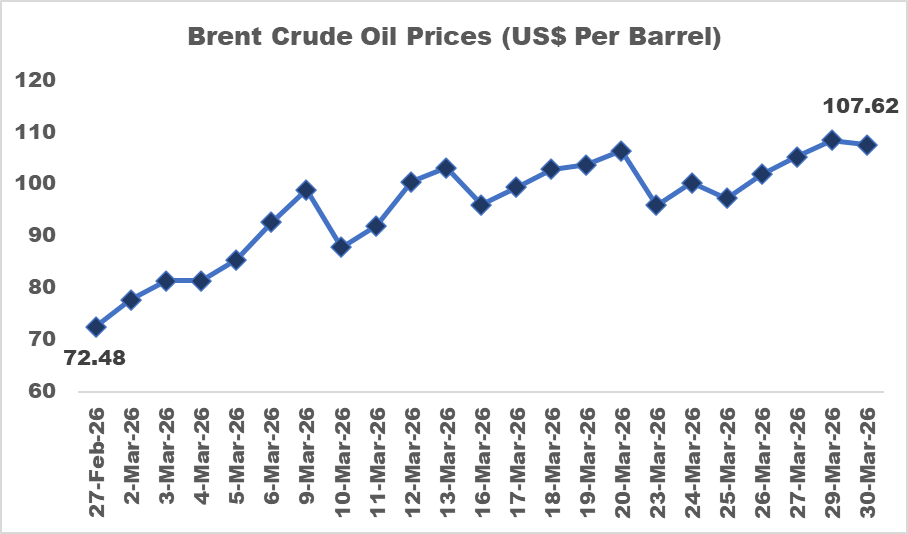

From what I have read about MTT, I think there are two major risks we need to look out for – ship fuel and ship maintenance costs.

I teased this out from looking at its cost structure in the previous point. Right now, the most urgent risk is its ship fuel costs due to the Iranian conflict. Brent crude oil prices have risen considerably since the outbreak of the conflict. And this will eat into MTT’s costs and gross profit margin.

Secondly, ship maintenance costs are always a dicey thing for shipping companies. You never quite know what to expect when it comes to repair and maintenance. Vessel costs after all, make up the biggest cost for MTT currently (soon, bunker fuel will make up the most with the rise in fuel prices).

#7: Outlook for MTT

I would say that MTT’s outlook is quite positive for the time being. There are two reasons why I believe so. Firstly, reading up about its supply and demand dynamics indicate that supply is tight in the industry right now. According to IMR (the consultant commissioned by MTT for its industry report),

“The expected shortage of ships, especially in the smaller size segments of below 4,000 TEUs, due to the expected increase in scrapping of non-compliant vessels over the next five years, is further compounded by the lack of foreseeable supply of container vessels in our segment, with the IMR estimating the order book ratio for ships below 4,000 TEUs at 14.6% by TEU capacity.”

In English, this means that MTT’s ships will be in high demand as there are not many other ships that are being supplied in the market currently. With more demand than supply, MTT should be able to charge higher freight rates moving forward.

MTT is also getting into the chemical and oil & gas industry transportation. It is currently commissioning two chemical tankers to come online by the end of 2026. This could serve the O&G industries in Bintulu, Miri and Kota Kinabalu and open up new markets for the company.

Conclusion

MTT Shipping and Logistics represents a transportation market leader for the West to East Malaysia route, that has had steady financial growth in the past couple of years. It has also rapidly expanded its market position in this route, further solidifying its competitive edge over its competitors.

There are risks however, especially from the shipping fuel front, where it might need to raise freight rates. However, that is mitigated by its market leader position where it can comfortably pass on the cost increases to its customers without affecting its position.