Interested in information and in-depth analysis on markets, investments and economies around the world? Subscribe to my newsletter here.

Disclaimer: This is not financial or investment advice. I take no responsibility for anyone’s decision regarding this.

Markets at a Glance

United States, S&P 500 (+2.3%): It has indeed been a good week for the U.S. markets. Negotiations between the U.S. and Iran are nearing another 60-day ceasefire. And U.S. companies’ results are soaring, especially in the AI software and hardware segments.

- The United States is ‘waiting’ for Iran’s response to the deal it has proposed. But as with all conflicts, the United States struck a couple of Iranian sites, while Iran also attacked some of the ships in the Straits of Hormuz. Investors are waiting for the finalisation of the ceasefire and looking forward to a longer-term deal.

- Top gainers in the market: Intel (+25%), Dell (+23.9%), Corning (+18.1%), Oracle (+14.0%), Qualcomm (+23.7%), Nvidia (+8.4%), Micron (+37.7%)

China, Hang Seng China Enterprise Index (+2.4%): In line with U.S. markets, the Chinese markets also rose by 2.4% on strong interest in their big tech companies plugged into the AI industry.

- Top gainers in the market: Kuaishou (+23.4%), Baidu (+22.3%), Alibaba (+10.3%), Xiaomi (+9.2%)

Malaysia, FBMKLCI (+1.5%): Well, Malaysia’s stock market rides the global trend too. It rose by 1.5% to settle near the 1,750 mark. Surprisingly, glove stocks made a comeback.

- Top gainers in the market: Public Bank (+4.3%), CIMB (+3.5%), Top Glove (+4.8%), Hartalega (+9.8%), Petronas Dagangan (+4.4%)

News Slices to Digest

Berkshire Hathaway’s New CEO, Greg Abel, Gives His First Press Conference

A new dawn is here for Berkshire Hathaway. Warren Buffett has retired last year, handing over the reins to Greg Abel. In his first press conference, he touched on a couple of things that are important for investors.

- What did he talk about mainly? He reassured investors that Berkshire Hathaway’s investment principles remain the same as when Warren Buffett and Charlie Munger (RIP) were in charge.

Other than that, you will be glad to know Berkshire’s first quarter in charge delivered exceptional results.

- How exceptional? Shareholder profits more than doubled from US$4.6 billion in 1Q 2025 to US$10.1 billion in 1Q 2026. It is now sitting on a massive cash pile of US$373 billion.

But what is Greg going to do with that cash pile? His press conference offers some clues to this that investors might be interested to know.

- What investment strategy? Firstly, he’s planinng to focus on Japanese markets. In the past few years, Berkshire Hathaway has been increasing its stake there, as they view the economic rebound (with inflation ticking up) as being real. There are also talks on whether Berkshire will insure ships passing through Straits of Hormuz. “It depends on the price” is the answer.

Spirit is Going Under Liquidation

Spirit Airlines is undergoing liquidation after it failed to reach a deal with the U.S. government to bail the company out. Bond holders of the company are now pushing for the company to sell its assets to repay them.

- Why is this important? Spirit has been loss-making since 2019, and JetBlue Airways tried to acquire the company for US$3.8 billion in 2022. But that deal was blocked by the government on antitrust grounds in 2024. Spirit’s unwinding will now involve thousands of workers being left without a job.

To Trump, this could have been a political win if the government decides to save Spirit. But as with all Trump deals, he wanted to squeeze the deal to its absolute limit and that’s where it fell apart when it was deemed too bad a deal.

- How is the industry dealing with this? Other airlines said that they will absorb the laid off workers from Spirit, but it’s not clear how many. But what’s certain is that the U.S. employment report will surely show this figures in their subsequent data releases.

Cerebras IPO

Another AI chip start-up going for a listing on the U.S. market. Cerebras is planning to raise up to US$3.5 billion with Morgan Stanley, Citigroup, Barclays and UBS as its book-running managers.

- Why is it listing? Cerebras is still trying to catch investors’ interest in the AI trend, as it makes processors customised for advanced AI models. Many companies are now transitioning from training to running them.

This timing also coincides with the deals that it has struck with OpenAI and Amazon recently.

- OpenAI: Will pay about US$20 billion over the next 3 years, to user servers powered by Cerebras chips.

- Amazon: Inference chip deal with Cerebras

Ford’s Aluminium Problem

Ford is paying more for aluminium, and it’s eating into its profit margins and production of cars. But this problem isn’t just unique to Ford, it’s hitting the whole auto industry in the United States.

- What happened? Because of the closure of the Strait of Hormuz, U.S. auto players lost aluminium supply from the Middle East. They constitute about one-fifth of U.S. imports of aluminium. Since then, global aluminium prices have been up by 17% to about US$3,575.

Ford and many other auto players use aluminium extensively to build the body of their cars. Ford faces much higher costs as one of its main suppliers in the U.S. shut down due to a fire.

- When will the plant be back? It’s reported that the aluminium plant will be back in production in June, but Ford expects that it will only ramp up eventually.

Despite this higher raw material costs, it has raised profit outlook for the year by US$500 million to US$8.5 billion to US$10.5 billion.

- Why is it optimistic? It expects its tariff refunds of about US$1.3 billion. Recall that the U.S. Supreme Court declared that Trump tariffs were illegal.

Palantir 1Q 2026 Results Soars Again

Palantir strikes again. 1Q 2026 financial results show that the company is delivering rapid revenue and profit growth.

- How rapid? Revenue is up by 85% to US$1.63 billion, while profits quadrupled to US$876 million. Most of these growth was driven by strong U.S. military demand and commercial demand for its data-crunching softwares.

This was a positive news for SaaS companies, as they suffered a shock earlier in the year. Investors were worried that AI could replace SaaS at lower costs and higher efficiency.

- What was Palantir’s value proposition? It essentially called AI software “AI Slop” and positioned its SaaS as softwares that can interpret data from multiple databases, and integrate themselves with other AI software.

DeepSeek Launches New AI Model, V4

The new V4 AI model reportedly is on the same level as U.S. rivals such as OpenAI and Anthropic. However, its impact is more far-reaching in the Chinese economic and stock market.

- How so? Several high-profile Chinese AI chipmakers such as Cambricon and Moore Threads stands to benefit significantly with higher AI chip demand. Other beneficiaries include MiniMax, Zhipu, Hua Hong, SMIC.

China’s AI chip market is projected to rise by 10x from CNY142.5 billion in 2024 to CNY1.34 trillion by 2029, according to Guotai Haitong Securities.

- What does this mean? It takes a very well-read investor in China’s market to realise this (I am not that person) – there’s a lot of hype right now for AI chip companies in China as the Chinese government is actively supporting the industry. But what happens when this support is taken away? The Chinese government has done the exact move to Chinese EV players recently. So, when will the government do the same for Chinese AI industry?

DeepSeek is also aiming to strengthen its market position in the AI market by reducing the prices on its AI model to only 3% of OpenAI’s price.

China’s Stranglehold on the Global Fertiliser and Pesticide Markets

This is a not-often known fact. China accounts for about one-third of global fertiliser production. And we only know that now because China has imposed export restrictions on fertiliser when the global market lost access to fertiliser coming through the Straits of Hormuz.

- Why? It is trying to keep most of its domestic fertiliser for its own farmers. It is also keeping the costs low to prevent a food inflation spiral in the agriculture industry. It has managed to keep urea’s price stable at US$300 per tonne compared to the global price of US$700 per tonne.

But that policy is also contributing to higher prices for fertilisers and pesticides. And this could potentially lead to higher food prices for the world. China produces 70% of the world’s raw materials for pesticides.

- Who will be affected? Brazil, Indonesia, Australia, Pakistan, Myanmar buy most of their phosphate fertiliser from China. Indirectly, other countries with extensive reliance on fertiliser and pesticides will be affected by higher global prices also.

Chinese EV Players Pivot Harder to Overseas Sales

It’s not just BYD; other Chinese electric vehicle players are pivoting hard toward overseas sales to boost finances and growth. The reasoning is straightforward – China’s domestic market is weak currently and the overseas market fetches higher profit margins. Here is how much other Chinese EV players are exporting in April 2026:

- BYD: 135,098

- Geely: 83,186

- Chery: 177,577

CK Hutchinson Sells Its Stake in Vodafone

Is it time to go on a buying spree? CK Hutchinson might be thinking that. It has divested its 49% stake in Vodafone for HK$45.6 billion.

- Why is it doing that? According to its chairman, Victor Li Tzar-kuoi, it wants to ‘build up a war chest’ where ‘rapid technological change and geopolitical complexity were creating fresh opportunities for mergers and acquisitions’. In English, it wants to invest in AI in the Hong Kong market, probably and avoid the problems that it had in the Panama Canal.

A bit of history on this investment. CK Hutchinson invested in Vodafone in the early days of 2000s when 3G connectivity was becoming more popular. Vodafone is now the biggest player in the UK’s telecommunications industry with the highest number of subscribers.

Pfizer Earnings Results for 1Q 2026

Covid-19 made and break Pfizer. Now, it’s investing in weight-loss and oncology drugs to make up its declining profits. 1Q 2026 results are out and its quite mixed to interpret.

- How was its results? Profit is down by about 10% to US$2.7 billion, due to Covid-19 vaccines revenue declining by 59%. However, its revenue is up by 5% due to higher sales from its blood-thinning drug, Eliquis.

Hence, Pfizer is now trying to regain its competitive edge in the market through acquiring Metsera, a weight-loss start-up for US$10 billion. It is also announcing its revenue and profit guidance.

- What is its guidance? Full-year 2026 revenue of US$59.5 billion to US$62.5 billion, and earnings per share of $2.80 to $3.00 per share.

AMD 1Q 2026 Earnings Results

AI hardware companies are having their Nvidia moment. AMD’s revenue grew by 38% to US$7.4 billion, while profits almost doubled to US$1.4 billion.

- What were the main drivers? AI data centre demand is growing at breakneck speed. Memory shortages are forcing companies to grab whatever computing power there is. Hence, that is great for AMD.

AMD has guided that the company will generate US$11.2 billion in revenue and that data centres have become the main engine for revenue.

- What did Lisa Su, CEO say? She has ‘strong and increasing confidence’ to reach tens of billions of dollars in data centre revenue “and to exceed our long-term growth target of greater than 80 percent in the coming years.”

Disney 1Q 2026 Earnings Results

With Bob Iger’s retirement, Josh D’Amaro has big shoes to fill. In its 1Q 2026 results, he outlines how the company performed and also what his plans are.

- How did Disney do? Not fantastic, not bad either. Revenue was up by 7%, but profits fell by 30%. Its streaming services, Disney+ and Hulu, recorded an 80% gain in their profits. However, that was dwarfed by a one-off tax benefit in 1Q 2025. Its theme park and linear television segments declined slightly.

Most importantly, he is pushing for a faster integration of technology into Disney’s business. He intends to use Disney+ as its core digital hub to push out content and video games. But there was a burning question regarding its linear television segment.

- Will Disney sell its linear TV segment? The answer is no. It cites that it’s complicated to sell its linear TV segment and is unsure whether it will give much value to shareholders.

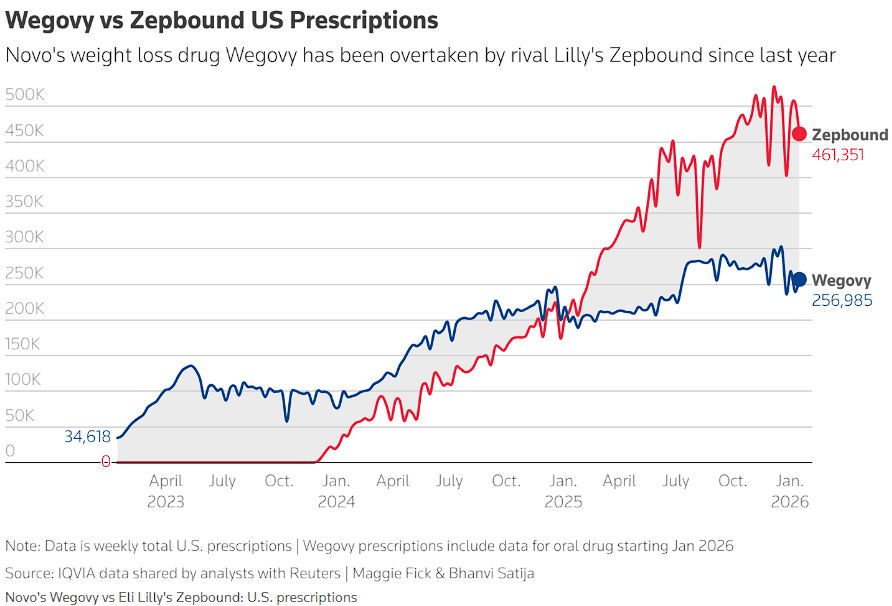

Novo Nordisk 1Q 2026 Results and its Position in the U.S. Weight Loss Market

Novo Nordisk used to be king with Ozempic. But it has been overthrown by Eli Lily. Now, it’s trying to regain lost ground in the U.S. market by focusing on its Wegovy weight-loss pill.

- How did it do in 1Q 2026? It exceeded expectations. Revenue grew by 24%, while profits were up by 67%. The decline in Ozempic sales wasn’t as bad. But generally, the weight-loss division makes up a small portion of its overall revenue.

Investors are keeping a close eye on this as they view the weight-loss market as the current boom trend in the healthcare industry.

- How has Novo Nordisk fared? It used to command the leading position in the market in 2023. But that position has been eroded by Eli Lily’s Zepbound in 2025.

It also faces pricing pressure as President Trump has pushed for lower medicine prices. Furthermore, patent protection for semaglutide is about to expire.

- Why is this important? With the expiration of the patent, other pharma companies can now produce generic drugs that are much cheaper. This will have an effect on Novo Nordisk’s prices for its weight-loss drugs.

Whirlpool in a Difficult Position after Delaying Dividend Payment

Whirlpool, an appliance maker, is facing severe financial difficulties after it has delayed its dividend payments to shareholders, citing ‘poor cash flow’.

- Why? Revenue has been declining for 4 straight years. It faces more competition from Samsung and LG. And it said that it didn’t pass on the raw materials price increases to consumers over the past few years. Now, it’s doing so. It is also blaming the Iran war for dampening consumers’ appetite in the United States. Though this point sounds like a poor excuse considering its poor financial track record.

Let’s look at its recent 1Q 2026 results. Revenue is down by 6.1%, dragged down by its North American division (-7.5%). However, its Latin American(+5.0%) and Global (+13.0%) divisions have been growing.

- How about its guidance? It has guided for a target revenue of US$15.0 billion for 2026, which is a 3% decline from 2025. Profits will be lower by half compared to 2025.

Stocks that I am Watching

There are two this week I am watching – one from the United States, one from China.

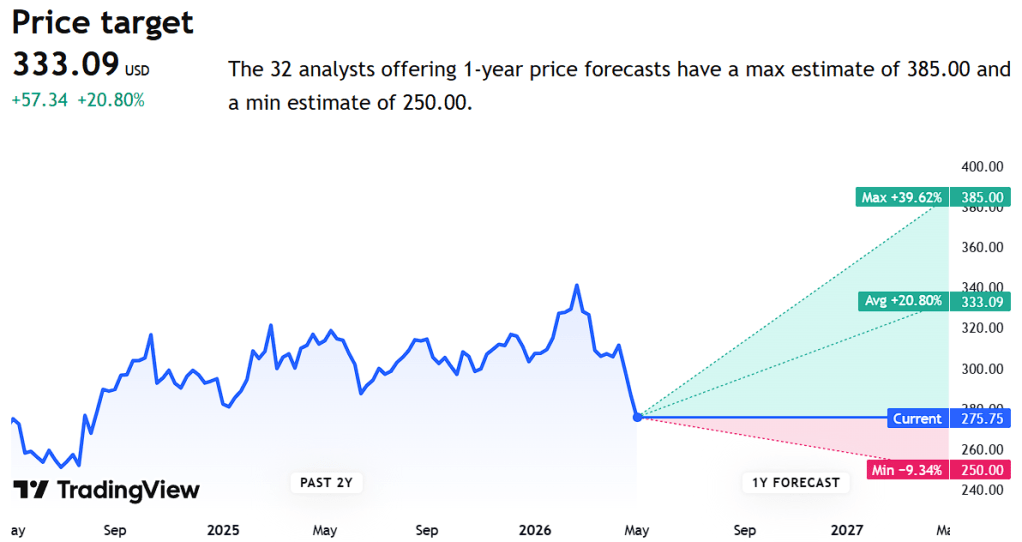

McDonald’s

I know what you are thinking about. McDonald’s? The fast-food chain giving ultra-processed food to the masses? But hear me out.

We all know that the U.S. economy is in a delicate state right now. It is at war. It faces inflation risks coming from higher crude oil and natural gas prices. The labour market is not too weak, not too great either.

But McDonald’s continued to grow from its latest 1Q 2026 results.

- Revenue is up by 9% to US$6.5 billion.

- Profits are also up by 6% to US$2.0 billion.

And it has managed to do this by doubling down on its budget meals. The U.S. economy is in a K-shape state now. Richer folks are spending more, but poorer folks are spending less. That’s where McDonald’s value offering is – cheaper budget meals for poorer households.

However, not all is honky dory. The company is facing higher costs from its beef section. I am sure you have heard about cattle prices recently rising to record highs. That’s why you see its profits growing less than its revenue.

- Its net profit margin has declined slightly to 30.4% in 1Q 2026 from 31.4% in 1Q 2025.

Valuation-wise, its price-to-earnings ratio of 23 times is now below its 5-year historical average of 27 times. According to analysts from Trading View, it has a potential upside of about +20.8%.

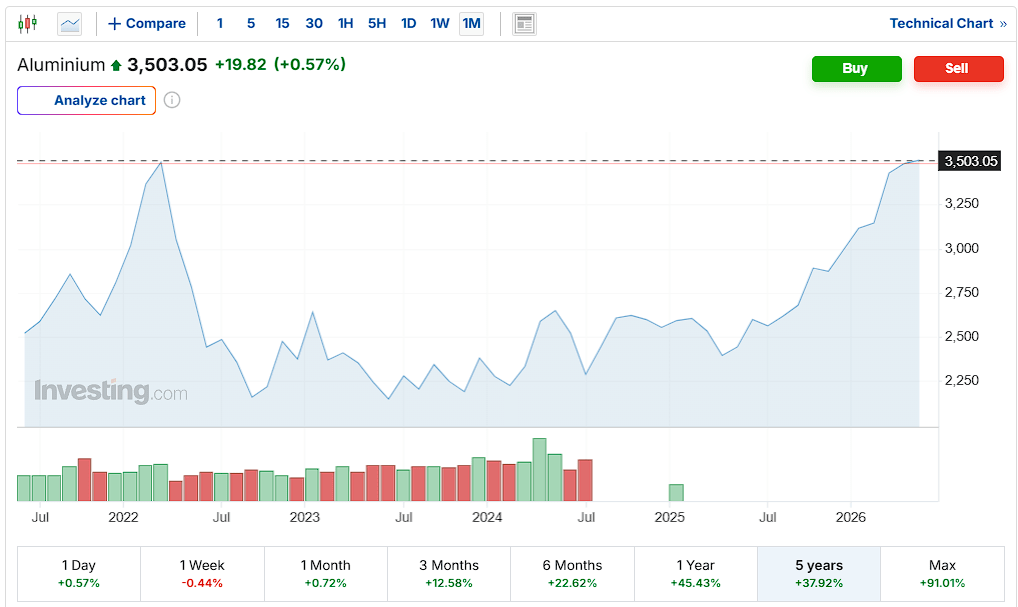

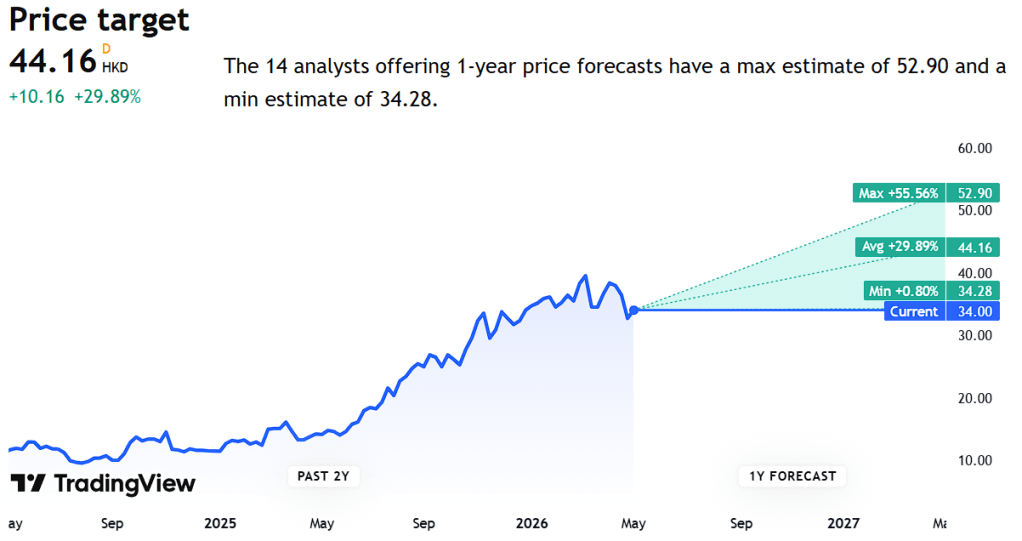

China Hongqiao Group

If you have never heard about this company, you might be in for a ride. China Hongqiao Group is China’s biggest aluminium products producer.

In the past month, share price has dropped by 10%, and it is now currently trading at a price-to-earnings ratio of 12.9 times. This is actually high compared to its historical average of around 5 to 7 times.

But the conflict in the Middle East has changed a lot of things. The supply of aluminium from that region has been disrupted and has lead to sky-high aluminium prices.

Prices are now riding a 5-year high.

Considering that it’s a market leader in China, this does indeed seem like an attractive opportunity. However, as in with all things, we need to balance it out against the risks.

- Prices are fickle. It’s high today but could be low tomorrow. Iran and the United States are already showing signs that it may be coming to a truce and that supply of aluminium could be recovering from the Middle East.

- A higher price for aluminium could be offset by higher freight and transportation costs.

Market analysts currently have the company at a target price of HKD 44.16 with a potential upside of +29.9%.

That’s all I have for this week.

Subscribe to my newsletter here for more news and analysis!